By Ahmed Tabaqchali, Chief Strategist of AFC Iraq Fund.

Any opinions expressed are those of the author, and do not necessarily reflect the views of Iraq Business News.

Markets Look Through Escalating Tensions

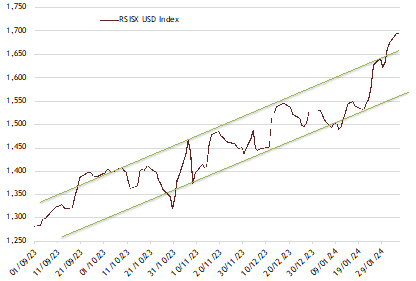

The market, as measured by the Rabee Securities U. S. Dollar Equity Index (RSISX USD Index), was up 8.8% for the month.

Over the last few months, fears of a widening of the Middle East conflict increased in line with the series of escalations that eventually led the US and the UK to take military action in the Red Sea, which intensified at the start of February following the US's strikes on targets in Syria and Iraq.

However, the Iraqi stock and currency markets, as well as oil markets, are discounting a very different outlook to that implied by these fears. Supporting the markets' different outlook are the US's clearly telegraphed and calibrated response, Iran's distancing itself from the attacks that led the US to act, a substate actor's declaration of the suspension of its attacks on US bases in Iraq even in the case of a US strike, and finally in that the US's strikes did not include targets in Iran.

Within Iraq, both the stock and currency markets were mostly discounting domestic dynamics that were driving the transformation of the economy, and that were already in place prior to the onset of the conflict in early October 2023. For the stock market, these dynamics were the expansionary 2023 budget, the continued growth in the money circulating in the economy, and the developments that promise to accelerate the adoption of banking and bring about a transformation of the sector and its role in the economy.

The RSISX USD Index's decline during the conflict's first month was a pull-back following a scorching four-month run in which it was up 43.7%, and not a reaction to the onset of conflict, as evidenced by the resumption of its rally in the following months while the conflict escalated. The index is up 20.9% from just before the start of the conflict to February 5th - in particular, it is up 4.4% since the attack on the US's base in Jordan on January 29th (chart below).

Rabee Securities U.S. Dollar Equity Index

(Source: Iraq Stock Exchange, Rabee Securities, AFC Research, data as of February 5th)

(Source: Iraq Stock Exchange, Rabee Securities, AFC Research, data as of February 5th)

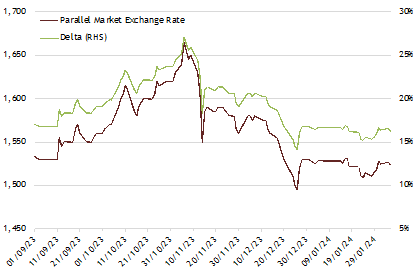

For the currency market, the dynamics were driven by the Central Bank of Iraq's (CBI) latest procedural requirements for its provisioning of U.S. dollars for cross-border transfers introduced in mid-November 2022, which led to a dollar supply-demand mismatch and consequently to the currency's upheaval (*). This upheaval was expressed as a depreciation of the parallel market price of the Iraqi dinar versus the dollar, or an increase in the delta between the parallel market exchange rate versus the dollar over the official exchange rate.

This delta increased from an average of around 1.2% that prevailed over the 18-month period preceding mid-November 2022 to 19.8% on the eve of the conflict. A month later, the delta increased to 27.1%, however, that was a function of the markets' ongoing adjustments to the mid-November 2022 procedural requirements, and not a reaction to the conflict itself. The delta subsequently narrowed to 16.3% by February 5th, as the parallel market price of the Iraqi dinar rallied by 8.5% against the dollar - an action that is hardly consistent with fears of a widening of the Middle East conflict that would come with capital flight, or dollar hoarding (chart below).

Dinar Parallel Market Exchange Rate vs. the Dollar and Its Delta over the Official Exchange Rate

(Source: Iraqi Central Statistical Organization, Iraqi Foreign Exchange Houses, Asia Frontier Capital Research,

(Source: Iraqi Central Statistical Organization, Iraqi Foreign Exchange Houses, Asia Frontier Capital Research,

data as of February 5th)

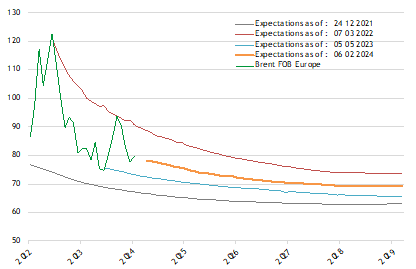

Finally, current oil market expectations, as measured by Brent crude futures contracts as of February 6th (yellow line-chart below), are near the middle of a range bound on the upper end by supply fears following the invasion of Ukraine (red line-chart below), and in the lower end, by those at the end of 2021 (grey line-chart below). Thus, while elevated, they are discounting a contained conflict, as discussed here a few months ago in "Assessing the Risks of a Wider Middle East Conflict".

Market Expectations for Future Oil Prices

As measured by Brent Futures Contacts (USD per barrel)

(Source: Wall Street Journal, US Energy Information Administration, AFC Research, data as February 6th)

(Source: Wall Street Journal, US Energy Information Administration, AFC Research, data as February 6th)

In conclusion, the Iraqi equity market, while beginning to discount the positive developments discussed in "What Next after a Gangbuster Year ???", is in the early phases of emerging from a brutal seven-year bear market in which RSISUSD index was down 66.6% during these years. Moreover, even after the stellar returns of 2023 and the strong start to 2024 it is, by end of January 2024, 19.7% below the all-time high achieved in early 2014 before the onset of the bear market. Risks to the Iraq story remain a factor given its history of conflict, extreme leverage to volatile oil prices, as well as the continued risks of an actual widening of the current Middle East conflict.

However, both fundamentally and technically, the risk-reward profile of the market remains very attractive compared with most global markets.

(*) Background to the currency's upheaval

The currency's upheaval was reviewed in prior market newsletters in: "Currency Upheavals Disrupt Market Activity" in January 2023; "Market Begins to Discount Currency Upheavals" in February 2023; "Dinar Revalued Upwards, Market Shrugs" in March 2023; "Tag Ends of Currency Upheaval Sparks Market Rally" in May 2023; and "Market Takes a Breather, While the Currency Stabilises" in June 2023. Further reviews on these and related issues are at: "Iraq needs to address the economy's structural imbalances to halt the dinar's volatility" in February 2023; "What's Happening with the Dinar?" in February 2023; and in "The Dinar, and the Conundrum over the Dollar and Iran" in August 2023.

Please click here to download Ahmed Tabaqchali's full report in pdf format.

Mr Tabaqchali (@AMTabaqchali) is the Chief Strategist of the AFC Iraq Fund, and is an experienced capital markets professional with over 25 years' experience in US and MENA markets. He is a Visiting Fellow at the LSE Middle East Centre, Senior Fellow at the Institute of Regional and International Studies (IRIS), and a Senior Non-resident Fellow at the Atlantic Council. He is also a board member of Capital Investments, the investment banking arm of Capital Bank in Jordan.

His comments, opinions and analyses are personal views and are intended to be for informational purposes and general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any fund or security or to adopt any investment strategy. It does not constitute legal or tax or investment advice. The information provided in this material is compiled from sources that are believed to be reliable, but no guarantee is made of its correctness, is rendered as at publication date and may change without notice and it is not intended as a complete analysis of every material fact regarding Iraq, the region, market or investment.

Comments are closed.