By Ahmed Tabaqchali, Chief Strategist of AFC Iraq Fund.

Any opinions expressed are those of the author, and do not necessarily reflect the views of Iraq Business News.

Market Takes a Breather, While the Currency Stabilises

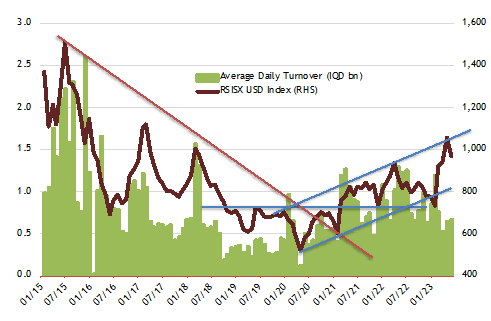

The market took a breather after a great three-month run from the January lows, during which it, as measured by the Rabee Securities RSISX USD Index, was up 43.8%. For the month the market was down 8.7% and up 24.9% for the year.

Its technical picture continues to be positive, with the pullback taking the index back to its three-year up-trending channel (first chart below). The macroeconomic fundamentals discussed here last year argue that this uptrend will likely remain in force; however, its upward slope might moderate or even go sideways as it consolidates its gains before its next move higher.

Supporting the consolidation thesis is the technical picture of the Rabee Securities RSISX IQD Index, the Iraqi Dinar (IQD) version of the Rabee Securities RSISX USD Index, which reflects a multi-month consolidation pattern (second chart below).

The fundamental underpinnings for the market's next move would come from the conclusion of parliament's review of the 2023 budget proposal and its passage into law, expected in the next few weeks. The expansionary budget, after coming into force, would result in meaningful liquidity injections into the economy as a consequence of the oversized role of the government's spending in the economy - which acts as an efficient and direct transmission mechanism of oil revenues into the real economy. Ultimately, this liquidity injection will feed into corporate profits, which in turn will provide the impetus for the market's next move.

RSISX USD, and RSISX IQD Indices versus Average Daily Turnover

(Source: Iraq Stock Exchange, Rabee Securities, AFC Research, data as of 31st May 2023)

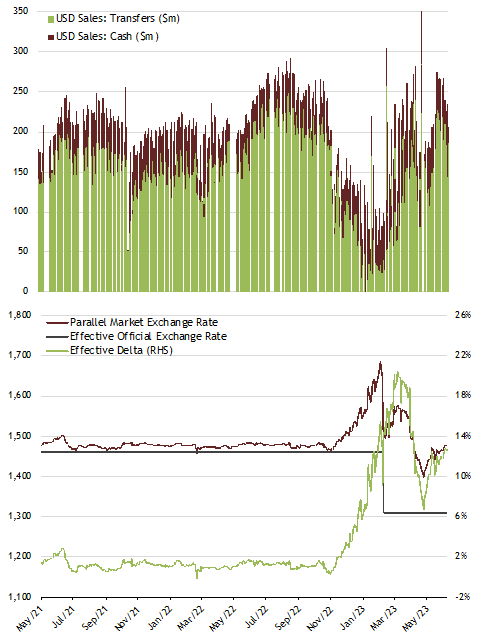

Meanwhile, following months of upheaval the currency is showing tentative signs of stabilisation, with the premium of the parallel market rate over the official rate of the IQD versus the USD trying to settle at around 13% versus the peak of around 20% and the recent low of about 7% (green line in the lower half of the chart below). At the same time, volumes in the Central Bank of Iraq's (CBI)'s daily USD-IQD transactions (upper half of chart below) continued to recover from the lows reached in November- which were brought about by the CBI's introduction of new procedural requirements to those for its provisioning of USD for cross-border fund transfers (*). Supporting this stabilisation is the combination of measures by the government and the CBI, to create demand for the IQD, and for furthering the adoption of banking in the economy - both of which have been increasingly gaining traction.

Volumes in CBI's USD-IQD Transactions versus the USD/IQD Exchange Rate

(Source: Central Bank of Iraq until 7th February 2023, Baghdad FX exchange houses from 8th February 2023, AFC Research, daily data as of 8h June 2023)

The current 13% premium of the parallel market exchange rate over the official exchange rate is a consequence of the informal sector's continued demand for USD that is not met at the official exchange rate through the banking system. Furthermore, it's too high versus the 1-2% levels that are consistent with a balanced supply-demand dynamic (green line in the lower half of chart above). As such, the 13% premium puts these informal companies at a significant competitive disadvantage versus those companies operating formally - accessing USD at the official exchange rate through the banking system. Consequently, providing the economic incentive for the informal companies to transfer to formality and to access the banking sector for the first time, which should drive the premium lower in tandem with the transfer to formality. However, the still high degrees of informality, cash, and the dollarization in economic activities mean that these developments will continue to unfold over time.

These incentives, and the high transparency levels demanded by the CBI's procedural requirements introduced in mid-November 2022, have benefited the higher-quality banks whose infrastructure is able to deal with the inflow of new clients and the subsequently increased volume of cross-border transactions. These developments are accelerating: (1) the shift away from informality that dominates the bulk of economic activities; and (2) the adoption of banking away from the dominance of cash as both a store of value and a means of economic exchange - a process that is positive for the investment thesis for the banking sector in Iraq as discussed here in "Banks & the Iraq Investment Thesis" in February 2022.

Notes

* Background to currency upheaval: As written here two months ago, the CBI, as part of an ongoing process of encouraging the move towards the adoption of banking and away from the informality that dominates economic activity, implemented in mid-November 2022 new procedural requirements to those for its provisioning of USD for importers. These procedural requirements would bring the country's cross-border fund transfers in-line with global standards, which require a high level of transparency. However, they represent a seismic shift to the country's cash-dominated economy, in which large informal sectors drive the bulk of economic activity. As such, the introduction of the new procedural requirements immediately affected the volumes of the CBI's daily USD-IQD transactions for cross-border fund transfers, which led to a supply-demand mismatch and consequently to a depreciation in the market price of the IQD versus the USD, and with that currency upheavals as discussed here over the last few months.

Please click here to download Ahmed Tabaqchali's full report in pdf format.

Mr Tabaqchali (@AMTabaqchali) is the Chief Strategist of the AFC Iraq Fund, and is an experienced capital markets professional with over 25 years' experience in US and MENA markets. He is a Visiting Fellow at the LSE Middle East Centre, Senior Fellow at the Institute of Regional and International Studies (IRIS), and a Senior Non-resident Fellow at the Atlantic Council. He is also a board member of Capital Investments, the investment banking arm of Capital Bank in Jordan.

His comments, opinions and analyses are personal views and are intended to be for informational purposes and general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any fund or security or to adopt any investment strategy. It does not constitute legal or tax or investment advice. The information provided in this material is compiled from sources that are believed to be reliable, but no guarantee is made of its correctness, is rendered as at publication date and may change without notice and it is not intended as a complete analysis of every material fact regarding Iraq, the region, market or investment.

Comments are closed.