By Ahmed Tabaqchali, CIO of Asia Frontier Capital (AFC) Iraq Fund.

Any opinions expressed are those of the author, and do not necessarily reflect the views of Iraq Business News.

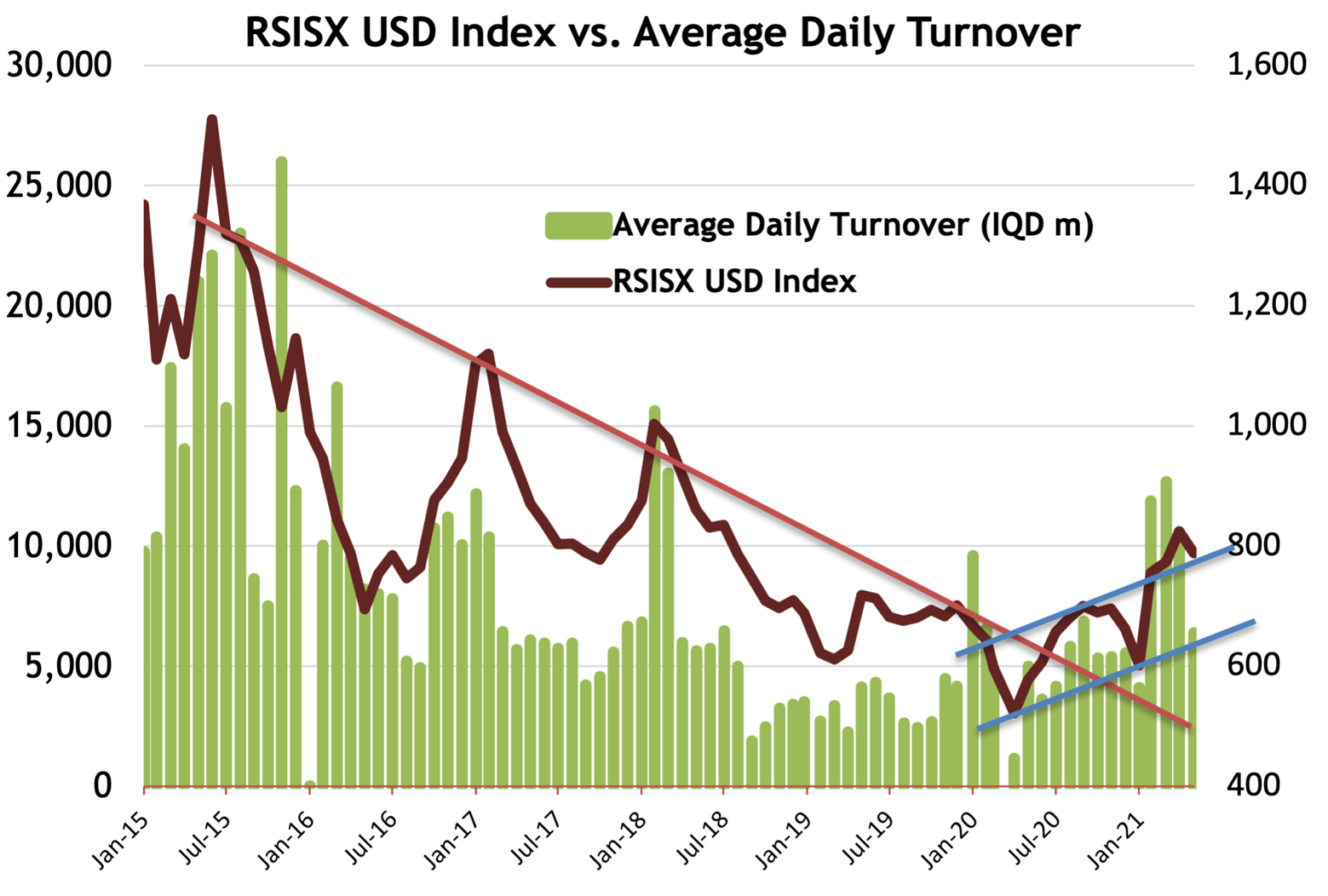

Market Review: "Market Consolidates Gains"

The market, as measured by Rabee Securities RSISX USD Index, paused its three-month string of gains in May, ending the month down 4.4%, which trimmed the year-to-date gain to 18.9%.

The market, throughout a much-shortened month - by a ten-day Eid holiday following the fasting month of Ramadan - followed through with the pattern of price declines on low turnover that started at the market's relative peak in the middle of last month.

The consistency of the declines on low turnover continues to suggest that the market is in the process of consolidating its recent gains within an up-trend (chart below).

(Source: Iraq Stock Exchange, Rabee Securities, Asia Frontier Capital, data as of May 31st)

Leading the index's action over the last few weeks, its leaders the Bank of Baghdad (BBOB), Pepsi bottler Baghdad Soft Drinks (IBSD), and mobile telecom operator AsiaCell (TASC) are in the process of consolidating their gains after blistering performances year-to-date.

In particular, IBSD was down 1.4% for the month after peaking mid-month, yet IBSD is still up 42.0% year-to-date, and up 148.8% from the severe decline in April 2020 as the market reacted to the twin shocks of the collapse in oil prices and the economic disruptions in the wake of COVID-19. While TASC was up 0.9% for the month after peaking a month earlier, it is still up 21.5% year-to-date, and 70.8% from the April 2020 low (chart below).

However, the disparity in performance between the two stocks is misleading as the Iraq Stock Exchange (ISX) does not adjust historic prices following dividend payments. TASC announced a dividend equivalent to a yield of 14.3% in July 2020, while IBSD announced a dividend equivalent to a yield of 5.6% in July 2020 and a further dividend corresponding to a 4.3% dividend yield in April 2021.

Adjusting for the dividend payments, IBSD provided a total return of 192.4% from the market's April 2020 low, while TASC provided a total return of 110.5% during the same timeframe (all price performance is in local currency terms).

Normalised returns for Baghdad Soft Drinks & AsiaCell

(Source: Bloomberg, data as of data as of May 31st)

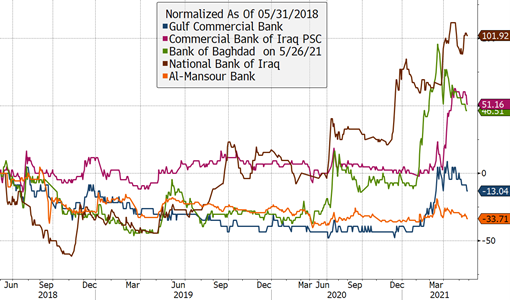

BBOB on the other hand, was down 3.0% for the month, having peaked a month earlier, yet it is up 66.7% year-to-date, and 140.0% from the April 2020 low. Within the leading banks, Commercial Bank of Iraq (BCOI) and Mansour Bank (BMNS) were respectively down 4.3% and 6.3% for the month; up 53.5% and 3.5% year-to-date; and 61.0% and 7.3% from the April 2020 lows.

The exception in the performance of the leading banks for the month was the National Bank of Iraq (BNOI) which was up 9.2%, up 28.2% year-to-date, and 109.6% since the April 2020 low (chart below). BNOI's performance from the lows in April 2020 reflects its strong performance in growing its deposit base and loan book compared to the other leading banks, as discussed in "Private Sector Deposit & Loan Growth Continues" in December 2020.

Joining the leading banks was lower-priced Gulf Commercial Bank (BGUC), which was down 13.0% for the month, but up 42.9% for the year and up 53.8% since the market's low in April 2020. The announcements of dividend equivalent to a yield 9.2% in March, 5.8% in February, and 6.6% in November by BNOI, BCOI and BMNS respectively changes their total returns from the April 2020 lows to gains of 147.7%, 71.4% and 15.7% (all price performances in local currency terms).

Normalised returns for Gulf Commercial Bank, Commercial Bank of Iraq, Bank of Baghdad, National Bank of Iraq, and Mansour Bank

(Source: Bloomberg, data as of data as of May 31st)

Strong price performance from the market's extreme COVID-19 lows are not unusual, however a continuation of such moves following the market's reaction to the devaluation in December 2020 is supportive of the argument made here then that "While the missing pieces of Iraq's re-rating are many and will take time to materialize, this positive reaction to the devaluation suggests that the event might start the process of Iraq's re-rating - which from a long-term perspective is positive for the equity market."

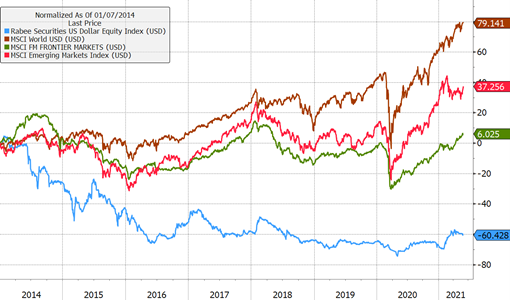

As such, the strong price performance discussed above should be seen from the perspective of an equity market that is emerging from a deep multi-year bear market in which the Iraqi equity market, as measured by the Rabee Securities RSISX USD Index, is still down about 62% from the 2014 peak. Therefore, from a risk-reward perspective, the Iraqi equity market is still very attractive versus other markets worldwide, most of which have had multi-year bull markets. Moreover, their recoveries from the April 2020 lows have surpassed their all-time highs, while the Iraqi equity market is just emerging from its multi-year lows.

Normalised returns for the RSISX USD Index vs MSCI World Index, MSCI Emerging Markets Index and MSCI Frontier Markets Index

(Source: Bloomberg, data as of data as of May 31st)

Please click here to download Ahmed Tabaqchali's full report in pdf format.

Mr Tabaqchali (@AMTabaqchali) is the CIO of the AFC Iraq Fund, and is an experienced capital markets professional with over 25 years' experience in US and MENA markets. He is a non-resident Fellow at the Institute of Regional and International Studies (IRIS) at the American University of Iraq-Sulaimani (AUIS), and an Adjunct Assistant Professor at AUIS. He is a board member of the Credit Bank of Iraq.

His comments, opinions and analyses are personal views and are intended to be for informational purposes and general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any fund or security or to adopt any investment strategy. It does not constitute legal or tax or investment advice. The information provided in this material is compiled from sources that are believed to be reliable, but no guarantee is made of its correctness, is rendered as at publication date and may change without notice and it is not intended as a complete analysis of every material fact regarding Iraq, the region, market or investment.

Comments are closed.