Tabaqchali: Iraqi Banks End the Year with a Bang

Posted on 04 April 2024 .

By Ahmed Tabaqchali, Chief Strategist of AFC Iraq Fund.

Any opinions expressed are those of the author, and do not necessarily reflect the views of Iraq Business News.

Banks End the Year with a Bang

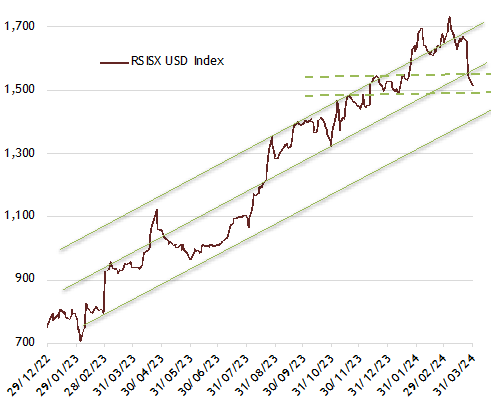

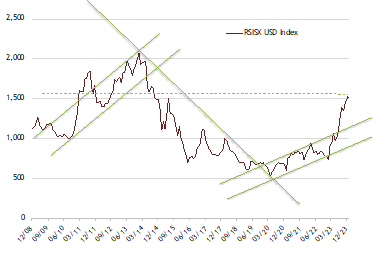

The market, as measured by the Rabee Securities U. S. Dollar Equity Index (RSISX USD Index), was down 8.4% for the month, and down 1.0% for the year. The onset of the fasting month of Ramadan at the end of the second week provided the market, and its participants, with a much-needed respite from the powerful momentum of the last few months, and an opportunity to consolidate the solid gains of this momentum (chart below) - with the extent of the consolidation influenced by the fundamentals that drove these gains.

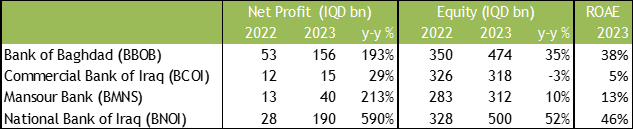

Key among them were the significant developments discussed a few months ago in "Banks to Fuel the Market's Next Phase", that would lead to an acceleration in the growth of net profit and equity values for the top quality banks. The extent of this acceleration can be seen from the stellar year-over-year growth in 2023 for country's top-four banks (table below)- which are among the RSISX USD Index's major constituents.

Rabee Securities U.S. Dollar Equity Index

(Source: Iraq Stock Exchange, Rabee Securities, AFC Research, daily data as of March 31st)

Year-over-Year Comparisons

(Source: Rabee Securities, AFC Research, data as of Q4/2023)

(Note: All numbers rounded up for ease of display, while percentage changes are of actual numbers)

The catalyst for this spectacular growth was the Central Bank of Iraq's (CBI) new procedural requirements for its provisioning of U.S. dollars for cross-border transfers in mid-November 2022, and the subsequent series of measures throughout 2023, which promise to accelerate the adoption of banking and bring about a transformation of the sector and its role in the economy. All of which disproportionally benefited the top-quality banks, whose net profit and equity values accelerated quarter on quarter from the 4th quarter of 2022 (Q4/2022), and throughout 2023 as the CBI's measures came into effect as discussed in the market outlook for 2024 in "What Next After a Gangbuster Year ???".

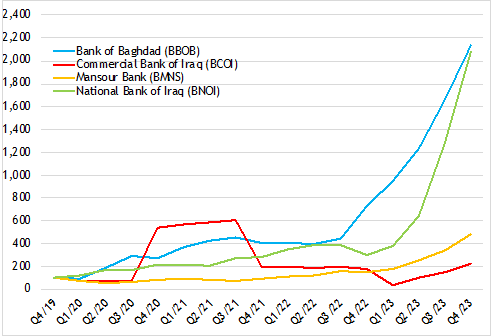

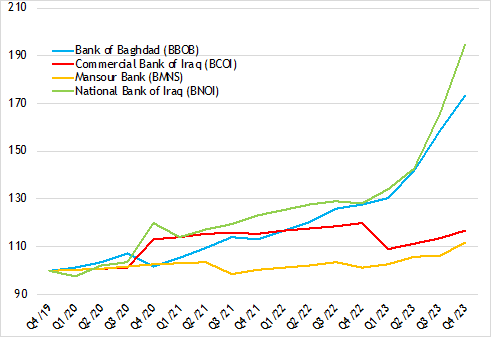

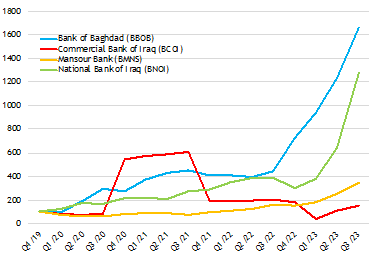

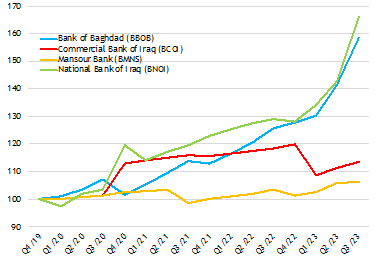

This acceleration can be appreciated by considering it in the context of the growth of each of these banks over the last four years as in the two graphs below. The first is that of trailing 12-month net profit, while the second is of trailing equity values, for Q4/19 - Q4/23. Both have been normalised, with Q4/19 figures set at 100 to allow for a review of the growth of these two key measures during this period, and for an easy comparison between the four banks - with the areas in pink background showing the effects of the acceleration that began in Q4/2022.

Normalised Trailing 12-months Net Profit

Normalised Trailing 12-months Equity Values

(Sources: Rabee Securities, AFC Research, data as of Q4/2023. Note: The graphs based on this data, are for net profit and equity value of the company and not per-share data.)

The National Bank of Iraq (BNOI), and the Bank of Baghdad (BBOB) both had a sharp acceleration in net profit and equity value quarter-on-quarter (above two charts), and both finished with stellar year-over-year growth for 2023 (above table). For the two banks, this growth builds upon the successful strategies pursued by each over the course of the prior few years as reviewed in "The Opportunity in Retail Banking" and in "Banks and the Predictability of Earnings".

Following these two, but with a distance, was Mansour Bank (BMNS), which still experienced strong growth, while the Commercial Bank of Iraq (BCOI) lagged the three, but nevertheless had a solid year-over-year growth in 2023 (*). For all of these banks, the accelerations in net profit and equity values builds upon the gradual multi-year recovery in the banking sector following the 2014-2017 economic crisis that devastated the sector, as reviewed in "Private Sector Deposit & Loan Growth Continues"; and in which each of the four bank pursued different strategies for recovery that drove each banks' growth trajectory.

The intensity of such an acceleration should moderate meaningfully over the course of the next few quarters, and the quarterly progression will likely be uneven, leading to a new normal for the net profit and equity value growth profile for each of the four banks. However, five strong quarters, i.e., Q4/22-Q4/23, are not enough to arrive at a picture of what this new normal is, as the CBI's measures would unfold over a long time - more likely measured in years than months - and importantly as the banks need to adapt their strategies and infrastructures to normalize these changes, and accommodate the higher growth levels.

Nevertheless, it's clear that the future growth trajectories of the four banks will be from a much higher base, and from a significantly improved financial position. Moreover, this new normal will be marked by an increased adoption of banking and of formality, coupled with a move away from the dominance of cash and informality - developments that the investment thesis for the banking sector contends would come with growth in bank lending, resulting in an expansion of the money circulating in the economy and consequently to an increase in non-oil GDP. Over time, the banks' net profit should grow substantially, and ultimately feed into higher stock market valuations driven by both earning momentums, and by increases in market multiples placed upon these net profits.

However, risks remain given Iraq's recent history of conflict, extreme leverage to volatile oil prices, as well as the risks of a potential widening of the current Middle East conflict that could destabilise the region - as reviewed recently in "Markets Continue to Look Through Tensions".

Notes

(*) The currency's official devaluation in December 2020, and subsequent revaluation in February 2023, had an over-sized effect on BCOI's net profit and equity values relative to the other three banks' net profit and equity values given the nature and size of its holdings of Iraq's sovereign Eurobonds - which has the effect of distorting the growth experienced in the period.

Please click here to download Ahmed Tabaqchali's full report in pdf format.

Mr Tabaqchali (@AMTabaqchali) is the Chief Strategist of the AFC Iraq Fund, and is an experienced capital markets professional with over 25 years' experience in US and MENA markets. He is a Visiting Fellow at the LSE Middle East Centre, Senior Fellow at the Institute of Regional and International Studies (IRIS), and a Senior Non-resident Fellow at the Atlantic Council. He is also a board member of Capital Investments, the investment banking arm of Capital Bank in Jordan.

His comments, opinions and analyses are personal views and are intended to be for informational purposes and general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any fund or security or to adopt any investment strategy. It does not constitute legal or tax or investment advice. The information provided in this material is compiled from sources that are believed to be reliable, but no guarantee is made of its correctness, is rendered as at publication date and may change without notice and it is not intended as a complete analysis of every material fact regarding Iraq, the region, market or investment.

Posted in Ahmed Tabaqchali, Investment Comments Off on Tabaqchali: Iraqi Banks End the Year with a Bang

IMF: Iraq Economic Growth "to Continue amid Fiscal Expansion"

Posted on 05 March 2024 .

By John Lee.

An International Monetary Fund (IMF) mission met with the Iraqi authorities in Amman during February 20-29 to conduct the 2024 Article IV consultation.

Some key data from their report:

- Economic Growth:

- Non-oil GDP growth: 6% in 2023.

- Overall growth projected to rebound in 2024.

- Inflation:

- Declined from 7.5% in January 2023 to 4% by year-end.

- Fiscal Position:

- Deficit: 1.3% of GDP in 2023, down from a surplus of 10.8% in 2022.

- Projected deficit for 2024: 7.6% of GDP.

- Public debt: Expected to nearly double from 44% in 2023 to 86% by 2029.

- Policy Priorities:

- Need for fiscal adjustment to stabilize debt and rebuild buffers.

- Focus on reducing current expenditure, increasing non-oil revenues, and improving revenue administration.

- Monetary Policy:

- CBI raised policy interest rates and reserve requirements.

- Efforts to reduce excess liquidity and improve monetary policy pass-through.

- Structural Reforms:

- Comprehensive employment strategy needed.

- Financial sector reform to improve credit access.

- Urgent pension reform required.

- Combat corruption and improve governance.

- Hurdles to private sector development need to be removed, including in the electricity sector and business registration procedures.

- IMF Support: The IMF staff team stands ready to support reform efforts.

Full statement from IMF:

An International Monetary Fund (IMF) mission, led by Mr. Jean-Guillaume Poulain, met with the Iraqi authorities in Amman during February 20-29 to conduct the 2024 Article IV consultation. The following statement was issued at the end of the mission:

Economic growth is projected to continue amid fiscal expansion. Meanwhile, medium-term vulnerabilities to oil price volatility have increased significantly. Reducing oil dependence and ensuring fiscal sustainability while protecting critical social and investment spending will require a significant fiscal adjustment, focused on controlling the public wage bill and increasing non-oil tax revenues. In parallel, higher economic growth will be needed to absorb the rapidly expanding labor force, boost non-oil exports and broaden the tax base. The authorities should therefore seek to enable private sector development, including through labor market reforms, modernization of the financial sector and restructuring of state-owned banks, pension and electricity sector reforms, and continued efforts to improve governance and reduce corruption.

Economic Outlook and Risks

Growth in the non-oil sector has rebounded strongly in 2023 while inflation receded. Supported by increases in public expenditure and solid agricultural output, real non-oil GDP is estimated to have grown by 6 percent in 2023 after stalling in 2022. Headline inflation declined from a high of 7.5 percent in January 2023 to 4 percent by year-end, reflecting lower international food and energy prices, and the impact of the February 2023 currency revaluation. The current account is expected to have recorded a surplus of 2.6 percent of GDP and international reserves increased to US$ 112 billion.

These positive developments were supported by the normalization of trade finance and the stabilization of FX market. After some initial disruptions following the introduction of new anti-money laundering and combating financing of terrorism (AML/CFT) controls on cross-border payments in November 2022, the improved compliance with the new system and the Central Bank of Iraq (CBI)'s initiatives to cut processing time led to a recovery in trade finance in the second half of 2023. This ensured private sector access to foreign exchange at the official rate for imports and travel purposes.

In the meantime, the fiscal position worsened. Although the expansionary budget was under-executed due to delayed Parliamentary approval, the fiscal balance still declined from a surplus of 10.8 percent of GDP in 2022 to a deficit of 1.3 percent in 2023, due to lower oil revenues and an increase in expenditures by 8 percentage points of GDP, of which salaries and pensions contributed 5 percentage points as the authorities started hiring in line with the budget law.

Overall growth is projected to rebound in 2024 and risks are tilted downwards amid heightened uncertainty. Non-oil growth momentum will continue in 2024. Larger declines in oil prices or extended OPEC+ cuts could weigh on fiscal and external accounts. If regional tensions escalate, a disruption of shipping routes or damage to the oil infrastructure could result in oil production losses that could outweigh the potential positive impact of higher oil prices. In case of a deterioration in domestic security conditions, this could lead to a decline in business sentiment and suspension of investment projects. Over the medium term, non-oil growth is projected to stabilize around 2.5 percent given existing hurdles to private sector development. Furthermore, vulnerability to oil price declines has increased as higher expenditures are projected to push the fiscal break-even oil price above $90 in 2024. Absent new policy measures, the fiscal deficit is expected to reach 7.6 percent in 2024 and widen further thereafter as oil prices are projected to gradually decline over the medium term. As a consequence, public debt would almost double from 44 percent in 2023 to 86 percent by 2029.

Policy Priorities

An ambitious fiscal adjustment would be required to help stabilize debt in the medium term and rebuild fiscal buffers, while protecting critical capital spending. Most of the fiscal adjustment would have to come from reducing current expenditure, especially controlling the wage bill by limiting mandatory hiring and gradually introducing an attrition rule. The authorities should also seek to increase non-oil revenues by broadening the personal income tax base and making it more progressive, reviewing the customs tariff structure, and considering new taxes on luxury items. In parallel, efforts to make revenue and customs administration more efficient should continue. Further savings could be obtained through better targeting social support and increasing cost recovery within the electricity sector. These adjustment measures should provide room for the expansion of the targeted social safety net.

The authorities should also strengthen public financial management and limit fiscal risks. The mission welcomes initial steps towards the establishment of a Treasury Single Account (TSA), which is crucial to improve cash management. Further progress is needed and close cooperation between the CBI and Ministry of Finance will be essential. The next steps are to define TSA design options and complete the bank account census. In future years, overall ceilings on the issuance of guarantees should be specified in the budget law and be enforced. The mission advise against the use of extrabudgetary funds and highlights potential fiscal risks associated with their use. As a second best, it would be important to ensure the Iraq Fund for Development has appropriate governance arrangements, including governing board independence while ensuring transparency of the Fund's activities including by publishing its investment plans in the annual budget documentation and restricting its ability to borrow.

The mission encourages the authorities to build on the CBI welcomed efforts to reduce excess liquidity. The CBI appropriately raised the policy interest rate and reserve requirements, introduced a 14-day CBI bill facility last summer, and scaled back its subsidized lending to the real estate sector. However, monetary policy pass-through has been muted, hampered by large excess liquidity and lack of market incentives in financial intermediaries, especially at state-owned banks. The CBI's ongoing efforts should be supported by consolidating idle government deposits in a TSA, refraining from procyclical fiscal policy, reducing the reliance on monetary finance, and improving public debt management. In parallel, efforts to develop an interbank market with the help of IMF technical assistance should continue. The mission also welcomes the authorities' steps to speed up the digitalization of the economy, reduce the reliance on cash and enhance financial inclusion.

Wide-ranging structural reforms are needed to foster private sector development and economic diversification. Iraq needs higher and more sustainable non-oil growth to absorb the rapidly growing labor force, increase non-oil exports and government revenue, and reduce the economy's vulnerability to oil price shocks. Key reform priorities include:

- Adopting a comprehensive employment strategy aimed at phasing-out mandatory hiring in the public sector, leveling the playing field between public and private jobs, addressing mismatches between educational curricula and the skills needed in the private sector, and strengthening labor market institutions. The strategy should also aim at reducing informality and addressing legal, social, and cultural impediments to women's participation in the workforce.

- Accelerating financial sector reform to improve access to credit. The authorities are committed to modernizing the banking sector and supporting banks' ability to secure correspondent banking relationships and have taken steps towards consolidation of small private banks. Efforts to restructure the two largest state-owned banks should intensify, including by expediting certification of past financial statements and implementation of core banking systems, and enhancing corporate governance in line with best practices.

- Implementing a comprehensive pension reform. This is urgently needed to reduce the overall projected fiscal costs of the public pension scheme, better align the benefits and rules across the public and private schemes, ensure adequacy of pensions and intergenerational equity, and increase the ratio of workers participating in the private pension scheme.

- Combating corruption and improving governance, particularly by strengthening the institutional and legal frameworks needed to ensure the independence of the Integrity Commission and the Board of Supreme Audit, enhancing the publication of assets and conflicts of interests declarations for top level officials, and adopting an updated anticorruption strategy. Further, public procurement and business regulations should also be enhanced. The authorities should also continue to strengthen the AML/CFT framework and its effectiveness, including in the banking sector, guided by the priority actions identified in the MENAFATF Mutual Evaluation that will be concluded in May 2024.

- Removing other hurdles to private sector development by reforming the electricity sector to improve efficiency, cost recovery, and reliable access; simplifying procedures for business registration; and upgrading critical infrastructure.

The IMF staff team stands ready to support the authorities in their reform efforts and would like to thank them for constructive and productive discussions during this mission.

(Source: IMF)

Posted in Iraq Industry & Trade News, Politics Comments Off on IMF: Iraq Economic Growth "to Continue amid Fiscal Expansion"

Tabaqchali: "What Next after a Gangbuster Year ???"

Posted on 08 January 2024 .

By Ahmed Tabaqchali, Chief Strategist of AFC Iraq Fund.

Any opinions expressed are those of the author, and do not necessarily reflect the views of Iraq Business News.

"What Next after a Gangbuster Year ???"

The market, as measured by the Rabee Securities U. S. Dollar Equity Index (RSISX USD Index), was up 6.2% and 97.2% for the month and the year, respectively, making it the best-performing equity market in the world.

After such a gangbuster year the obvious question is what is in store for the market in 2024? The answer lies with the drivers of the market's performance in 2023 and their continuation going forward. The key driver was a significant fundamental development that promises to accelerate the adoption of banking and bring about a transformation of the sector and its role in the economy as discussed a few months ago in "Banks to Fuel the Market's Next Phase".

The catalyst for this development was the Central Bank of Iraq's (CBI) new procedural requirements for its provisioning of U.S. dollars for cross-border transfers in mid-November 2022. These were part of an ongoing process of encouraging the economy's increased adoption of banking; they nevertheless represented a seismic shift to the country's cash-dominated economy, in which large informal sectors drive the bulk of economic activity.

As such, their introduction had an immediate detrimental effect on the volumes of cross-border transfers conducted through the CBI, which led to a dollar supply-demand mismatch and consequently to the currency's upheaval (i).

In the ensuing months, the CBI introduced a raft of measures to further regulate cross-border transfers, accelerate the adoption of banking and the use of the banking system for settling commercial transactions instead of cash. These measures, coupled with the unintended consequences of the currency's upheaval, created the economic incentives for informal companies to transfer to formality and to access the banking sector for the first time (ii).

The CBI followed these by two key measures that would substantially strengthen the banking system and advance its development. The first measure was the mandate that that all banks should increase their capital by up 60% by the end of 2024, after which the CBI would initiate a merger, an acquisition, or a liquidation of banks that fail to comply. The second measure was that all cross-border-transfers in 2024 would be through banks that have foreign correspondent banking relationships, bringing the process fully in-line with that of the rest of the world.

These two measures, on top of the earlier ones, have disproportionally benefited the top-quality banks, who have the wherewithal to increase their capital bases, who already have correspondent banking relationships with major international banks, and whose infrastructures are able to deal with the meaningful inflows of new banking customers and the subsequent increased volumes of cross-border transactions.

A preview of the resultant boost to the earnings growth of four of the top-quality banks that are among the RSISX USD Index constituents, as the CBI's measures came into effect throughout 2023, can be seen in the last three quarterly reports for these banks. The extent of this boost can be appreciated by considering these reports, i.e. the first quarter of 2023 (Q1/23) to Q3/2, in the context of the growth profiles over the last five years as in the two graphs below.

The first is that of trailing 12-month earnings, while the second is of trailing book values, for Q4/19 - Q3/23. Both have been normalised, with Q4/19 figures set at 100 to allow for a review of the growth of these two key measures during this period, and for an easy comparison between the four banks.

Normalised Trailing 12-months Earnings

Normalised Trailing 12-months Book Values

(Sources: Rabee Securities, AFC Research. See (iii) below for further information)

(Sources: Rabee Securities, AFC Research. See (iii) below for further information)

Among the four banks, the Bank of Baghdad (BBOB) and the National Bank of Iraq (BNOI) experienced sharp accelerations in earnings and book values throughout 2023, reflecting the successful strategies pursued by each over the course of the last few years as reviewed here last year in "The Opportunity in Retail Banking" and in "Banks and the Predictability of Earnings". Mansour Bank (BMNS), to a much lesser extent, experienced faster growth throughout 2023, while the Commercial Bank of Iraq (BCOI) lagged, but still had higher growth during the year (iv). For these banks, these accelerations build upon the gradual multi-year recovery in the banking sector following the 2014-2017 economic crisis that devasted the sector, as reviewed in "Private Sector Deposit & Loan Growth Continues".

While such acceleration in quarterly earnings growth has turbo-charged the recent trends in earnings growth, however, the intensity should moderate meaningfully over the course of the next few quarters. Nevertheless, both earnings and book values should continue to grow strongly from a higher base, as the full effects of the CBI's measures unfold over a long time given the economy's still high levels of informality.

Thus, providing a boost to the investment thesis for the banking sector, the thrust of which is that increased adoption of banking would come with growth in bank lending, resulting in an expansion of the money circulating in the economy and consequently to an increase in non-oil GDP. Over time, banks' earnings should grow substantially, leading to meaningful increases in their valuations, and ultimately feed into much higher market multiples.

Among other drivers for the market's performance in 2023 was the cumulative positive effects of the relative stability that the country has enjoyed over the last few years, which provided a more stable and predictable macroeconomic framework for businesses and individuals to operate in and plan for capital investments on a scale not seen in the prior decades of conflict (v). Another driver was the positive macro backdrop that allowed the government to pursue expansionary policies that should boost economic growth and, ultimately, corporate profits, as discussed in "Government Starts Implementing Expansionary 2023 Budget".

The Iraqi equity market, while beginning to discount the fundamental developments discussed above, is in the early phases of emerging from a brutal seven-year bear market in which the RSISX USD Index was down 25.4% in 2014, 22.7% in 2015, 17.4% in 2016%, 11.8% in 2017, 15% in 2018, 1.3% in 2019, and -5.4% in 2020 - for a cumulative decline of 66.6%. Even after the 97.2% increase in 2023, it is still 26.2% below the all-time high achieved in early 2014 before the onset of the bear market.

However, risks to the Iraq investment story remain given its recent history of conflict, extreme leverage to volatile oil prices, as well as the risks of a potential widening of the current Middle East conflict that could destabilise the region - as reviewed recently in "Assessing the Risks of a Wider Middle East Conflict".

Rabee Securities U.S. Dollar Equity Index

(Source: Iraq Stock Exchange, Rabee Securities, AFC Research, data as of January 4th)

(Source: Iraq Stock Exchange, Rabee Securities, AFC Research, data as of January 4th)

Notes.

- The currency's upheavals were reviewed in prior market newsletters in: "Currency Upheavals Disrupt Market Activity" in January 2023; "Market Begins to Discount Currency Upheavals" in February 2023; "Dinar Revalued Upwards, Market Shrugs" in March 2023; "Tag Ends of Currency Upheaval Sparks Market Rally" in May 2023; and "Market Takes a Breather, While the Currency Stabilises" in June 2023. Further reviews on these and related issues are at: "Iraq needs to address the economy's structural imbalances to halt the dinar's volatility" in February 2023; "What's Happening with the Dinar?" in February 2023; and in "The Dinar, and the Conundrum over the Dollar and Iran" in August 2023.

- Following the implementation of the CBI's new procedural requirements, the premium of the parallel market exchange rate over the official exchange rate increased significantly from the average of 1.2% that prevailed over the 18-month period preceding mid-November 2022. It traded between a low of 2.0% soon after mid-November 2022 to a high of 27.5% in early November 2023, and ended 2023 at 16.5% --with an average of 14.4% for the period. Such a high premium created a huge competitive advantage for companies operating formally versus those operating informally -consequently providing the economic incentive for informal companies to transfer to formality and to access the banking sector for the first time.

- Data provided by Rabee Securities are based on company filings of un-audited quarterly reports between Q1/19 to Q3/23. The calculations based on this data, are for net earnings and book value of the company and not per-share data.

- The currency's official devaluation in December 2020, and revaluation in February 2023, had an over-sized effect on BCOI's earnings and book values relative to the other three banks' earnings and book values given the nature and size of its holdings of Iraq's sovereign Eurobonds - which has the effect of distorting the growth experienced in the period. Moreover, unlike the other three banks, BCOI had a correspondent banking relationship indirectly through its majority owner and as such didn't benefit in the same way as the other three did. However, it should have established a direct correspondent banking relationship and can stand to benefit more - but will be limited somewhat by its capacity constraints. BCOI's ultimate majority regional owner is Kuwait Finance House, the second largest Islamic bank globally by assets, after its merger with BCOI's original owner Al Ahli United Bank.

- One of the most promising recent developments in the economy is the meaningful capital investment by businesses and individuals, brought about by the relative stability of the last five years following the end of the ISIS conflict. While these years were punctured by several shocks, such as the countrywide demonstrations in late 2019, the assassination of Iran's top general in Baghdad followed by the emergence of COVID-19 and the crash in oil prices in 2020, the undecisive elections in 2021, followed by a year of a political impasse topped by political conflict and violence in the summer of 2022. Nevertheless, these shocks were short-lived, and did not lead to self-reinforcing cycles of violence and conflict along the lines of the past. As such, this relative stability provided a more stable and predictable macroeconomic framework for businesses and individuals to operate in, and to plan for capital investments on a scale not seen in the last prior decades of conflict; that in turn, should be sustained by the population's pent-up demand for goods and services to catch up with the rest of the world. These developments were reviewed in prior market reports:

-

- "Construction Activity and Stability", in July 2023.

- "Supermarkets and Stability", in December 2022.

Please click here to download Ahmed Tabaqchali's full report in pdf format.

Mr Tabaqchali (@AMTabaqchali) is the Chief Strategist of the AFC Iraq Fund, and is an experienced capital markets professional with over 25 years' experience in US and MENA markets. He is a Visiting Fellow at the LSE Middle East Centre, Senior Fellow at the Institute of Regional and International Studies (IRIS), and a Senior Non-resident Fellow at the Atlantic Council. He is also a board member of Capital Investments, the investment banking arm of Capital Bank in Jordan.

His comments, opinions and analyses are personal views and are intended to be for informational purposes and general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any fund or security or to adopt any investment strategy. It does not constitute legal or tax or investment advice. The information provided in this material is compiled from sources that are believed to be reliable, but no guarantee is made of its correctness, is rendered as at publication date and may change without notice and it is not intended as a complete analysis of every material fact regarding Iraq, the region, market or investment.

Posted in Ahmed Tabaqchali, Investment Comments Off on Tabaqchali: "What Next after a Gangbuster Year ???"

IMF: Iraq Economic Activity is Recovering

Posted on 21 December 2023 .

By John Lee.

A team from the International Monetary Fund (IMF) has concluded a visit with Iraqi officials, concluding:

- Economic activity is recovering, although oil production cuts are weighing on overall growth, and at the same time inflation has declined.

- The large fiscal expansion in the three-year budget law poses significant risks to fiscal and external sustainability over the medium term.

- Fiscal prudence and structural reforms are critical to safeguard macroeconomic stability, ensure sustainability, and achieve durable and more inclusive growth.

Full statement from the International Monetary Fund:

A staff team of the International Monetary Fund (IMF) led by Jean-Guillaume Poulain met with the Iraqi authorities in Amman, Jordan during Dec 12-17 to discuss recent economic developments and outlook as well as policy plans.

At the end of the mission, Mr. Poulain issued the following statement:

"Against the background of a large fiscal expansion, non-oil GDP is expected to grow by 5 percent in 2023. Continued budget execution should help sustain strong non-oil growth in 2024. However, lower oil production, following the closure of the Iraq-Turkey pipeline and OPEC+ production cuts, will reduce overall GDP growth in 2023 and 2024. Inflation has declined from its January peak and is projected to stabilize in the coming months-helped by the Central Bank of Iraq's (CBI) tighter monetary policy, passthrough from the exchange rate revaluation, lower international food prices, and normalization of trade finance as compliance to the new anti-money laundering/combating the financing of terrorism (AML/CFT) framework improved.

"The three-year budget approved in June 2023 marked a shift in Iraq's budgeting practice, envisaged to improve fiscal planning and continue important development projects over the medium term. Despite a late start of budget implementation, the fiscal balance is expected to shift from a large surplus in 2022 to a deficit in 2023. Staff projects that the deficit would widen further in 2024 reflecting the full year impact of recent measures. The large fiscal expansion, including a substantial increase in public hiring and pensions creates permanent spending that will put pressure on public finances over the medium term.

"Ensuring fiscal sustainability, in context of uncertain outlook for oil prices, requires gradually tightening the fiscal policy stance while safeguarding critical infrastructure and social spending needs. This would require mobilizing additional non-oil revenues, containing the large government wage bill, and reforming the pension system. These measures should be supported by moving toward a more targeted social safety net that better protects the vulnerable.

"The mission welcomed the government's plans to strengthen public financial management including steps towards the establishment of the Treasury Single Account. In this context, the mission reiterated the importance of adhering to the framework for managing government guarantees.

"The CBI has appropriately tightened its monetary policy, including by increasing its policy rate and reserve requirement. The mission welcomed the progress in strengthening the domestic liquidity management framework and encouraged continued efforts to mop up excess liquidity and develop an interbank market to strengthen monetary policy transmission.

"Structural reforms to spur private sector led economic diversification and job creation remains pivotal for sustainable and inclusive growth. Priorities include creating a level playing field for the private sector through banking and electricity sector reforms, reducing distortions in the labor market, and continuing efforts to enhance governance and reduce corruption.

"The IMF staff team stands ready to support the authorities in their reform efforts and would like to thank them for candid and productive discussions during this mission."

(Source: IMF)

Posted in Iraq Industry & Trade News, Politics Comments Off on IMF: Iraq Economic Activity is Recovering

Iraq Maintains its S&P Credit Rating

Posted on 07 September 2023 .

By John Lee.

In the latest credit rating report by Standard & Poor's (S&P), Iraq has retained its credit rating at B- / B with a stable outlook.

According to the statement from the Ministry of Finance, the report highlights Iraq's financial and economic stability.

It continues:

"This new rating reflects Iraq's continued economic and financial reform policies, led by the Ministry of Finance. It also acknowledges Iraq's ability to maintain foreign currency reserves exceeding external public debt while meeting other external financial obligations, thanks to stable crude oil prices.

"The report considers several key indicators, including the Iraqi Parliament's approval of the three-year budget (2023-2025) aimed at revitalizing infrastructure projects and economic needs. It also notes that the formation of the government in late 2022 has contributed to political stability.

"Furthermore, the report predicts a significant surplus in the current account within the economic forecasts, adding to the strong foreign currency reserves, ultimately supporting Iraq's external debt service capabilities over the next 12 months.

"S&P anticipates that economic growth will reach 2.6% annually during the years 2023-2026, driven by increased oil production and its impact on non-oil sector growth. In addition, annual inflation rates are expected to decrease to 4% in July 2023, compared to 5-6% in 2021 and 2022. This reduction is attributed to government measures involving currency revaluation, price control, and government support for food and energy prices.

"The agency suggests that Iraq's credit rating could improve if economic growth rates rise, government revenue diversifies both from oil and non-oil sources, and individual income shares increase from the national income. Continuous financial and economic policy reform is also seen as a positive factor."

(Source: Ministry of Finance)

Posted in Investment, Iraq Banking & Finance News, Politics Comments Off on Iraq Maintains its S&P Credit Rating

IMF Forecasts Growth in Iraq's Real Non-Oil GDP of 3.7%

Posted on 06 June 2023 .

By John Lee.

The International Monetary Fund (IMF) has forecast growth in Iraq's real non-oil GDP 3.7 percent in 2023.

Following a recent visit to Iraq, the IMF team also predicts inflation of 5.6 percent in for the year.

Full statement from IMF:

A staff team of the International Monetary Fund (IMF) led by Tokhir Mirzoev visited Amman, Jordan from May 24-31 to discuss with the Iraqi authorities the recent economic developments and outlook as well as policy plans in the period ahead.

At the end of the mission, Mr. Mirzoev issued the following statement:

" The Iraqi economy's growth momentum has slowed in recent months. After recovering to its pre-pandemic level last year, oil production is set to contract by 5 percent in 2023 owing to the OPEC+ production cut and outage of the Kirkuk-Ceyhan oil pipeline. The foreign exchange (FX) market volatility in the wake of tighter anti-money laundering/combating the financing of terrorism (AML/CFT) controls by the Central Bank of Iraq (CBI) on FX sales has adversely affected import-dependent non-oil sectors. Real non-oil GDP is estimated to have contracted by 9-percent (year-on-year) in the last quarter of 2022, negating its growth during the previous three quarters. With the FX market appearing to be stabilizing, helped by CBI's actions, growth of real non-oil GDP is expected to resume and reach 3.7 percent in 2023. After spiking to 7 percent in January, inflation has begun to moderate-reflecting lower international commodity prices as well as a 10-percent revaluation of the dinar-and is projected to average 5.6 percent in 2023.

"Favorable oil market conditions have supported Iraq's fiscal and external positions, but structural imbalances continue to widen. In 2022, fiscal and external current account surpluses have reached 7.6 and 17.3 percent of GDP respectively on the back of record-high oil revenues. The CBI's FX reserves rose to US$97 billion (11 months of imports), including US$16.3 billion (6 percent of GDP) in fiscal savings accumulated by the government. At the same time, a large fiscal expansion has widened the non-oil primary deficit from 52 to over 68 percent of non-oil GDP in the course of 2022.

" An even bigger fiscal loosening envisaged in the draft 2023 budget law would widen the non-oil primary fiscal deficit further to 75 percent of non-oil GDP and bring the overall fiscal balance to a deficit of 6.5 percent of GDP. The combined effects of increased government spending, the exchange rate revaluation, and reduced oil production would bring the fiscal break-even oil price to $96 per barrel.

" In the short run, implementation of the authorities' fiscal plans could re-ignite inflation and FX market volatility. Over the medium term, continuation of current policies in the presence of substantial uncertainty about the future path of oil prices poses critical macroeconomic stability risks. Barring a large increase in oil prices, the current fiscal stance could lead to mounting deficits and intensifying financing pressures in the coming years.

"A significantly tighter fiscal policy is needed to strengthen resilience and reduce the government's dependence on oil revenues while safeguarding critical social spending needs. Key priorities include diversifying fiscal revenues, reducing the oversized government wage bill, and reforming the pension system to make it financially sound and more inclusive. While supporting the government's plan to increase social assistance, the mission recommends stronger targeting to ensure that it is directed to those who are most vulnerable.

"Improving public financial management remains of critical importance. In this context, the mission cautions against the planned establishment of new extrabudgetary funds, which raise governance and efficiency concerns, and strongly recommends adhering to on-budget government expenditures Furthermore, the mission urges full implementation of the framework for managing government guarantees, including Parliamentary approval and publication of an annual ceiling on and the list of government guarantees as part of the budget law. Accelerated efforts to establish a Treasury Single Account are also needed to strengthen public financial management.

"The mission welcomes the progress made by the CBI in improving its liquidity management and the AML/CFT frameworks and underscores the importance of close alignment of the stance of fiscal and monetary policies in managing the economy.

"Creating an enabling environment for private sector development will be of utmost importance for achieving durable and more inclusive growth. Priorities include continued efforts to enhance governance and reduce corruption, restructuring large state-owned banks to improve access to finance, reforming the labor market to promote private sector job creation, improving cost recovery in the electricity sector to enhance its ability to meet demand in a sustainable manner, and improving the broader business environment.

"The IMF staff team stands ready to support the authorities in their reform efforts and would like to thank them for candid and productive discussions during this mission."

(Source: IMF)

Posted in Iraq Industry & Trade News, Iraq Oil & Gas News, Politics Comments Off on IMF Forecasts Growth in Iraq's Real Non-Oil GDP of 3.7%

Tabaqchali: Dinar Revalued Upwards, Market Shrugs

Posted on 12 March 2023 .

By Ahmed Tabaqchali, Chief Strategist of AFC Iraq Fund.

Any opinions expressed are those of the author, and do not necessarily reflect the views of Iraq Business News.

Iraq Market Report: Dinar Revalued Upwards, Market Shrugs

The market, as measured by the Rabee Securities RSISX USD Index, was up 24.9% in February, and up 18.8% for the year. However, this strong performance was positively affected by two crucial decisions taken by the Central Bank of Iraq (CBI).

The first was a revaluation, in early February, of the official exchange rate of the Iraqi Dinar (IQD) versus the US Dollar (USD) by 10.3% or from USD 1 = IQD 1,450 to USD 1 = IQD 1,300. The second was the implementation of its recent measures to widen access to the official rate and to remove bureaucratic barriers for the transfer of funds to/from Iraq, as discussed here a few months ago. The combination effectively means that most transfers to/from Iraq will be affected at the effective official rate of USD 1 = IQD 1,290/1,320 instead of the parallel market rate of USD 1 = IQD 1,552/1,562 at month end, and as such the official exchange rate would be the rate to be used for the valuation of the index going forward - both of which explains the strong monthly performance.

Adjusted for the CBI's measures, in other words, if the currency had been flat at February's close, then the RSISX USD Index's would have declined 2.1% for the month - this underling decline, coupled with the 36.0% month-on-month decline in the average daily traded volume on the Iraq Stock Exchange (ISX), suggests that the market has largely shrugged off the effects of the IQD's 10% revaluation against the USD and that it has continued with its looking through and discounting the currency's volatility as discussed last month.

The RSISX USD Index's performance is mirrored in those of its constituents, especially considering the strong performance of a number of constituents last month which this month had minor declines. In local currency terms, only the Bank of Baghdad (BBOB) was up 2.1%, Asiacell (TASC) almost flat at -0.1%, and the rest were down. The decliners were led by Al-Mansour Hotels down 8.1%, Kharkh Tour Amusement City (SKTA) down 5.5%, Al Mansour Bank (BMNS) down 4.5%, Baghdad Soft Drinks (IBSD) down 4.2%, the National Bank of Iraq (BNOI) down 3.8%, the Commercial Bank of Iraq (BCOI) down 1.9%, Iraqi for Seed Production (AISP) down 1.8%, and Al-Mansour Pharmaceutical Industries (IMAP) down 1.4%.

The revaluation of the IQD versus the USD and the valuation of the index at the official exchange rate going forward, has not fundamentally altered the technical picture of the market, as it is now halfway through its 34-month up-trending channel reversing most of the negative effects of the currency's declines since mid-November 2022 (chart below) - which still supports the market's positive technical picture as discussed here in the past few months. The macroeconomic fundamentals discussed here last year support our view that this uptrend will likely remain in force; however, its upward slope might moderate or even go sideways - as the effects of the CBI's measures would not affect the coming months' market action. The 2023 budget proposal was not submitted in January 2023 as expected, nor in February 2023 as hoped for, but hopefully will be submitted this month or the following month - which means a delayed catalyst for the market's next move - especially as all indications suggest that it would be a much more expansionary budget that was discussed here a few months ago.

RSISX USD Index versus Average Daily Turnover

(Source: Iraq Stock Exchange, Rabee Securities, AFC Research, data as of March 9th)

(Source: Iraq Stock Exchange, Rabee Securities, AFC Research, data as of March 9th)

Revaluation of the Iraqi Dinar versus the US Dollar

Background: As written here last month, the Central Bank of Iraq (CBI), as part of an ongoing process of encouraging the move towards the adoption of banking and away from the informality that dominates economic activity, implemented in mid-November 2022 new procedural requirements to those for its provisioning of USD for importers. These procedural requirements would bring the country's cross-border fund transfers in-line with global standards which require a high level of transparency. However, they represent a seismic shift to the country's cash-dominated economy, in which large informal sectors drive the bulk of economic activity. As such, the introduction of the new procedural requirements immediately affected the volumes of the CBI's daily USD-IQD transactions for cross-border fund transfers, which led to a supply-demand mismatch and consequently to a depreciation in the market price of the IQD versus the USD.

The government and the CBI subsequently introduced a sequence of measures to create demand for the IQD and for furthering the adoption of banking - crucial measures to de-dollarize the economy, and to accelerate its evolution away from the dominance of cash. As crucial as these measures are, their full effectiveness will take place over several years, and as such, the IQD's market prices versus the USD continued to decline. Given public pressures, spurred by populist rhetoric, for immediate measures, the CBI, with the government's blessing, implemented a 10 per cent revaluation of the IQD exchange rate against the USD - from 1,450 to 1,300 IQDs per USD - in the hope that the market price of the IQD would reverse its depreciation versus the USD.

Fundamentally, the revaluation in nominally lowering the official exchange rate does not alter the relationship between the official exchange rate and the market rate that existed pre-revaluation - a relationship that reasserted itself with the premium of the market rate over the official rate staying at the same elevated levels as those pre-revaluation (green line in lower half of chart below).

Volumes in CBI's USD-IQD Transactions versus the USD/IQD Exchange Rates

(Source: Central Bank of Iraq until February 7th, Baghdad FX exchange houses from February8th, AFC Research, daily data as of March 9th)

(Source: Central Bank of Iraq until February 7th, Baghdad FX exchange houses from February8th, AFC Research, daily data as of March 9th)

While the revaluation was nominal, yet the combination with the CBI's measures - that eased onerous bureaucratic processes for cross border-fund transfers at the official USD-IQD exchange rate, and the creation of incentives for the adoption of banking away from the prevalence of cash in economic transactions and payments - has accelerated the move away from informality that dominates the bulk of economic activities. The 22% premium of the market exchange rate over the official exchange rate (lower half of chart above) created a huge competitive advantage for companies operating formally versus those operating informally - consequently providing the economic incentive for informal companies to transfer to formality and to access the banking sector for the first time. These developments, and the high transparency levels demanded by the CBI's procedural requirements introduced in mid-November 2022, have benefited the higher-quality banks whose infrastructure is able to deal with the inflow of new clients and the subsequent increased volumes of cross-border transactions. Moreover, they have accelerated the adoption of banking away from the dominance of cash as both a store of value and a means of economic exchange - a process that is positive for the investment thesis for the banking sector in Iraq as discussed here in "Banks & the Iraq Investment Thesis" in February 2022.

Consequently, the volumes of the CBI's USD-IQD transactions have begun to recover from the lows at the end of the prior year and began a gradual upward trend, helped by the market's on-going adjustment to the increased levels of transparency demanded in cross-border fund transfers (first half of above chart). However, the still high degrees of informality, the dollarization in economic activities and the time needed for the market to fully adjust to the increased levels of transparency demanded in cross-border fund transfers, mean that volumes will likely remain lower than the pre-November 2022 levels - when the CBI's new measure for cross-border fund transfers was first introduced. Consequently, the pressures on the market price of the exchange rate of the IQD versus the USD will likely continue, however, these will ease in time and the premium over the official rate will likely stabilize in a range that is lower than the current high levels.

Please click here to download Ahmed Tabaqchali's full report in pdf format.

Mr Tabaqchali (@AMTabaqchali) is the Chief Strategist of the AFC Iraq Fund, and is an experienced capital markets professional with over 25 years' experience in US and MENA markets. He is a Visiting Fellow at the LSE Middle East Centre, Senior Fellow at the Institute of Regional and International Studies (IRIS), and a Senior Non-resident Fellow at the Atlantic Council. He is also a board member of Capital Investments, the investment banking arm of Capital Bank in Jordan.

His comments, opinions and analyses are personal views and are intended to be for informational purposes and general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any fund or security or to adopt any investment strategy. It does not constitute legal or tax or investment advice. The information provided in this material is compiled from sources that are believed to be reliable, but no guarantee is made of its correctness, is rendered as at publication date and may change without notice and it is not intended as a complete analysis of every material fact regarding Iraq, the region, market or investment.

Posted in Ahmed Tabaqchali, Investment, Iraq Banking & Finance News, Politics Comments Off on Tabaqchali: Dinar Revalued Upwards, Market Shrugs

Iraq Restores Value of Dinar

Posted on 07 February 2023 .

By John Lee.

The Iraqi authorities have approved a revaluation of the Iraqi dinar.

In a statement said on Tuesday, the Central Bank of Iraq (CBI) said that, starting on Wednesday, the exchange rates will be as follows:

- 1,300 dinars per dollar: the price of purchasing a dollar from the Ministry of Finance;

- 1,310 dinars per dollar: the selling price of the dollar to banks through the electronic platform; and,

- 1,320 dinars per dollar: the sale price of the dollar from banks and non-bank financial institutions to the final beneficiary.

The dinar had fallen as low as 1,470 dinars per dollar in recent days, causing increased prices for imported goods.

(Sources: Govt of Iraq, CBI)

Posted in Iraq Banking & Finance News, Iraq Industry & Trade News, Politics 2 Comments

Possible Revaluation of the Iraqi Dinar?

Posted on 04 November 2022 .

By John Lee.

Iraqi Prime Minister has reportedly told a press conference that his government intends to increase the value of the Iraqi dinar (IQD) against the US dollar.

Kurdistan24 quotes Mohammed Shia al-Sudani as saying that the interests of the needy were not taken into consideration when the currency was devalued by approximately 20 percent in December 2020. "We tend not to repeat that in this cabinet," he said.

But according to Asharq al-Awsat, even though more than 50 MPs have petitioned the government to reverse the devaluation, it is considered unlikely to happen, as it would increase the government's costs by more than $24 billion each year.

Al Araby also cites the Iraqi Finance Minister as saying that the dinar value will not be changed in the 2023 budget bill.

It adds, however, that former Prime Minister Nouri Al Maliki has suggested an exchange rate of 1,375 dinars per dollar, down from the current level of 1,460, but not back to the pre-devaluation level of 1,182.

(Sources: Kurdistan24, Asharq al-Awsat, Al Araby)

Posted in Investment, Iraq Banking & Finance News, Iraq Industry & Trade News, Politics Comments Off on Possible Revaluation of the Iraqi Dinar?

Central Bank of Iraq: "No Future Plan to change Exchange Rate"

Posted on 11 July 2022 .

By John Lee.

The Central Bank of Iraq (CBI) has said that there is no justification for changing the exchange rate of the Iraqi dinar relative to the US dollar.

CBI Deputy Governor, Ammar Khalaf, confirmed to the official Iraqi News Agency (INA) that, "in our belief as a monetary authority, there is no justification for changing it ... changing the exchange rate remains within the monetary authority's policy and according to circumstances."

He repeated that economic circumstances are the main criterion, and "there is no future plan to change the exchange rate ... there is no justification or need to modify it."

Since the change of regime in Iraq in 2003, many unsophisticated investors in the United States have been persuaded to buy Iraqi dinars in the hope of stratospheric upward revaluations.

See also:

https://www.iraq-businessnews.com/2012/08/29/7-questions-for-dinar-speculators/

https://www.iraq-businessnews.com/2012/08/06/you-cant-fix-stupid-the-iraqi-dinar-scam/

https://www.iraq-businessnews.com/2012/07/04/iraqi-dinar-investments-opportunity-or-scam/

Posted in Iraq Banking & Finance News, Iraq Industry & Trade News 1 Comment